ill Tax Cuts in 2026 actually boost American households, or will the benefits flow upward again? A deep analysis of income, inflation, debt, and real purchasing power.

Table of Contents

Introduction: Relief or Illusion?

Few policy tools generate as much political excitement as tax relief. As Washington debates new Tax Cuts scheduled to shape the 2026 fiscal landscape, supporters promise higher take-home pay, stronger consumer spending, and renewed economic confidence.

But many Americans are skeptical—and for good reason.

Despite years of market growth and multiple rounds of tax changes, household finances remain under pressure. Inflation has eroded wages, housing costs remain elevated, and debt burdens continue to rise. This raises a critical question: will 2026 Tax Cuts truly help households, or will they mainly inflate asset prices and corporate profits once again?

What the 2026 Tax Cuts Are Aiming to Do

At their core, the proposed changes focus on:

- Extending or modifying existing personal income reductions

- Adjusting standard deductions and child-related credits

- Offering targeted relief to middle-income earners

- Preserving incentives for business investment

The political narrative is straightforward: leave more money in people’s pockets so they can spend, save, and invest.

However, the economic reality is far more complex.

The Difference Between Paper Gains and Real Gains

A lower tax bill does not automatically translate into improved living standards.

Real household benefit depends on:

- Inflation-adjusted income

- Cost of essentials (housing, healthcare, food, education)

- Debt servicing costs

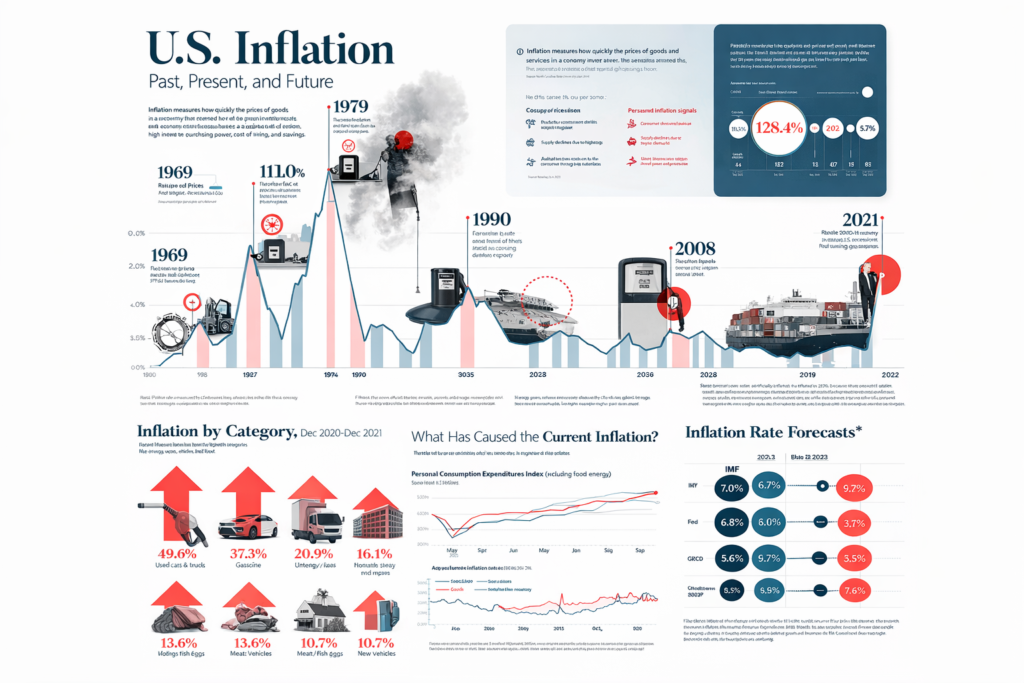

The Bureau of Labor Statistics consistently shows that nominal income growth often looks healthier than real purchasing power once inflation is considered

(https://www.bls.gov).

This distinction matters when evaluating whether Tax Cuts actually improve day-to-day life.

Who Typically Benefits the Most?

Historically, tax changes tend to deliver uneven outcomes.

Higher-income households often:

- Save or invest tax savings

- Benefit from capital gains and asset appreciation

- Experience compounding wealth effects

Lower- and middle-income households, by contrast:

- Use tax savings to cover rising costs

- See benefits absorbed by inflation

- Gain little long-term financial security

According to analysis from the Congressional Budget Office, broad tax reductions often deliver a disproportionate share of benefits to top earners unless tightly targeted

(https://www.cbo.gov).

Inflation: The Silent Offset

Even modest inflation can erase the impact of Tax Cuts within months.

If households receive lower withholding but face:

- Higher rent

- Rising insurance premiums

- Increased food and energy costs

the net effect may feel negligible.

The Federal Reserve has repeatedly warned that fiscal stimulus without productivity growth can add inflationary pressure rather than real income gains

(https://www.federalreserve.gov).

This is why many Americans report feeling poorer even after nominal tax relief.

The Debt Factor Most Debates Ignore

Household debt has quietly become one of the biggest constraints on financial well-being.

Credit cards, auto loans, student debt, and mortgages absorb much of any extra cash households receive. In practice, Tax Cuts may simply help families service debt rather than build wealth.

The Federal Reserve Bank of New York shows that rising interest rates have sharply increased household debt payments since 2023

(https://www.newyorkfed.org).

Debt reduces the multiplier effect policymakers hope tax relief will create.

Consumption vs Financial Security

From a macroeconomic standpoint, governments often want households to spend tax savings to boost growth.

But households increasingly prioritize:

- Emergency savings

- Debt reduction

- Healthcare and education buffers

This shift reflects economic anxiety, not confidence.

When people save tax relief instead of spending it, the short-term growth impact is limited—though household resilience improves slightly.

Will Tax Cuts Boost Wages?

One common argument is that business-oriented tax relief eventually raises wages through investment and productivity gains.

Evidence here is mixed.

While some firms reinvest savings, others:

- Increase buybacks

- Raise executive compensation

- Hold cash amid uncertainty

The International Monetary Fund has noted that wage growth following tax reductions is often slower and smaller than promised

(https://www.imf.org).

Without strong labor bargaining power, wage benefits remain uncertain.

Regional and Demographic Differences

Not all households experience tax changes equally.

- Homeowners benefit more than renters

- Families with children gain more from credits

- High-cost states feel less relief due to housing and healthcare expenses

This uneven distribution complicates claims that Tax Cuts broadly boost American households.

Markets vs Households: A Familiar Pattern

Financial markets typically respond positively to tax reductions. Investors anticipate higher profits and stronger earnings.

But as seen repeatedly, market optimism does not guarantee household relief. Asset owners gain faster than wage earners.

This dynamic has fueled distrust in economic policymaking and widened the perception gap between economic indicators and lived reality.

The Long-Term Fiscal Trade-Off

Tax relief today often means higher deficits tomorrow.

If cuts are not offset by growth or spending discipline, future households may face:

- Reduced public services

- Higher indirect taxes

- Increased borrowing costs

The U.S. Treasury has warned that sustained deficits limit fiscal flexibility during future downturns

(https://home.treasury.gov).

Short-term relief can create long-term constraints.

So, Will 2026 Tax Cuts Really Help?

The honest answer: partially, unevenly, and temporarily.

Some households will feel modest relief, especially those benefiting from targeted credits. Others will see gains quickly eroded by inflation and rising costs.

Without complementary policies—housing supply, healthcare affordability, productivity investment—Tax Cuts alone are unlikely to transform household finances.

What Would Make Tax Cuts More Effective?

For tax relief to meaningfully help households, it must be paired with:

- Inflation control

- Wage growth policies

- Affordable housing expansion

- Reduced healthcare cost pressure

Tax policy works best as part of a broader economic strategy—not as a standalone solution.

Conclusion: Relief Isn’t the Same as Recovery

Tax reductions are politically attractive because they are visible and immediate. But economic well-being is shaped by deeper structural forces.

In 2026, Tax Cuts may ease pressure for some households—but they are unlikely to reverse years of cost increases, debt accumulation, and inequality on their own.

For many Americans, real prosperity will depend less on tax bills and more on whether everyday costs finally stop rising faster than paychecks.

The gap between Wall Street vs Main Street is widening. This deep-dive explains why stock markets soar while everyday Americans struggle with inflation, debt, and stagnant wages.